I recently ran into a neighbor who wanted to know if it makes more sense to sell or rent her home in June when her last child graduates high school.

So here we are—this blog is for her and anyone else wrestling with the same decision! As brokers who handle both sales and rentals, we get this question ALL. THE. TIME. Many of us are sitting on incredibly low interest rates (us included!), and the idea of renting or selling can feel like a real dilemma. Let’s break it down together.

Selling vs. Renting: The Pros & Cons

Selling:

- Pro: Cash out your equity NOW—upgrade to a bigger home or free up funds for other investments.

- Pro: No landlord headaches—no tenant maintenance, no legal risks.

- Con: You lose your low interest rate.

- Con: You may owe significant capital gains taxes (approx. 20-24% Federal + 10% CA—check with your CPA for specifics).

Renting:

- Pro: Hold onto your home as an appreciating asset, while locking in today’s low rate; Rental income can cover costs and even generate positive cash flow.

- Pro: “Try before you sell”: Rent for up to 3 years and still keep your $500K capital gains exclusion if you’ve lived in the home for 2 out of the past 5 years. If you rent long-term, you can still defer taxes using a 1031 Exchange when you sell later.

- Con: You take on landlord duties—maintenance, management fees, tenant risks.

- Con: Converting your home to a rental means you may lose the ability to transfer your low tax basis (55+ homeowners) under Prop 19 if you move later.

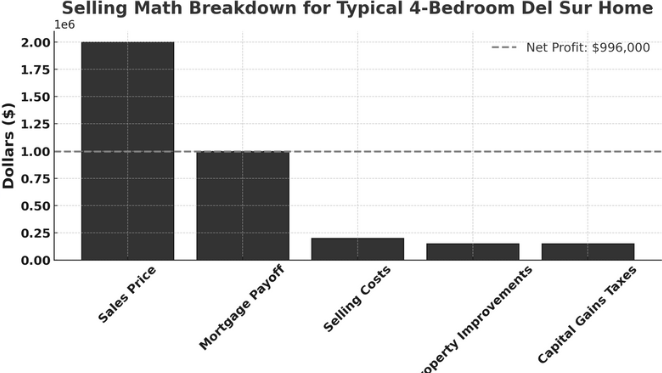

Here’s an example of how selling might look for a 4-bedroom Del Sur home purchased in 2015:

- Sales Price: $2,000,000

- Purchase Price: $800,000

- Mortgage Balance: $640,000

- Selling Costs (6% total): $120,000

- Property Improvements: $100,000

- Capital Gains Exemption (married): $500,000

Step-by-Step Calculation:

- Cash at closing: $2,000,000 - $640,000 - $120,000 - $100,000 = $1,140,000.

- Taxable Portion: Sales Price - (Purchase Price + Improvements + Selling Costs): $2,000,000 - ($800,000 + $100,000 + $120,000) = $980,000

- Subtract the $500K exemption: $980,000 - $500,000 = $480,000 taxable.

- Capital Gains Tax (30% combined): $480,000 × 30% = $144,000.

Net Profit:

$2,000,000 - $640,000 (mortgage) - $120,000 (costs) - $100,000 (improvements) - $144,000 (taxes) = **$996,000**.

Here's how the sale profit breaks down:

Renting Math Breakdown

Now, let’s look at renting out the same home instead:

- Rent Income: $5,800/month

Annual Costs:

- Mortgage (3%): $32,000

- Insurance: $3,500

- Property Taxes (including Mello Roos): $20,000

- HOA: $2,400

- Management Fees (10%): $6,960

- Leasing Fee: $3,500

- Maintenance/Repairs (2%): $6,400

Key Financial Metrics:

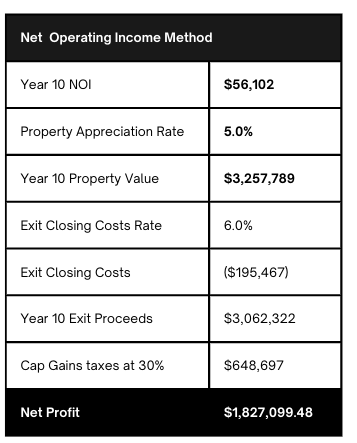

- Cap Rate = Net Operating Income (NOI) ÷ Property Value (San Diego averages 2.5%; reaching 7% by Year 10 is excellent.)

- Appreciation: At a conservative 5% annual rate: $2,000,000 × (1.05)^10 = **$3,257,789** value in 10 years.

After taxes and closing costs, you could still see an additional $1,827,099 in net profit.

However, here’s the tradeoff:

- After 3 years, your $500K capital gains exemption begins to phase out.

- After 5 years, you lose it entirely, resulting in higher taxes when you sell.

- You also lose the ability to transfer your low tax basis if you’re over 55.

Decision Time

Ultimately, this decision comes down to your personal goals:

- Sell if: You need cash for a larger or smaller home, or you don’t want the responsibilities of being a landlord.

- Rent if: You want to hold onto your home as an appreciating asset and are comfortable managing tenants.

Ready to Chat?

I know that was a lot of information (and math!), but that’s what we’re here for—to walk you through the numbers, options, and next steps. Whether you’re ready to sell, rent, or just explore your options, let’s talk. We’ve got the spreadsheets, the expertise, and maybe even a cup of coffee waiting for you.